Login

Login

The day-to-day operation of all 401(k) plans must be governed by a written plan document that meets Internal Revenue Code requirements. Occasionally, 401(k) plan documents will require an amendment to reflect law changes or employer intentions. The Internal Revenue Service (IRS) has strict rules for plan amendments. It’s important for employers to understand them. Otherwise, they could miss the chance to make discretionary plan changes, accidentally cut back protected benefits, or face punishment for document non-compliance. It’s not difficult for employers to stay out of trouble. While 401(k) amendment rules are strict, they are generally straightforward. Below are some basics.

General amendment deadlines

401(k) plan amendments can be either “interim” or “discretionary” in nature. Interim amendments are required to update a plan document for recent law changes, while discretionary amendments are voluntary. These amendment types have different adoption deadlines:

- Interim amendments – must be adopted (signed and dated) no later than the end of the second calendar year following the calendar year in which the change in qualification requirements is effective.

- Discretionary amendments - must be adopted by the last day of the plan year that includes the amendment’s effective date.

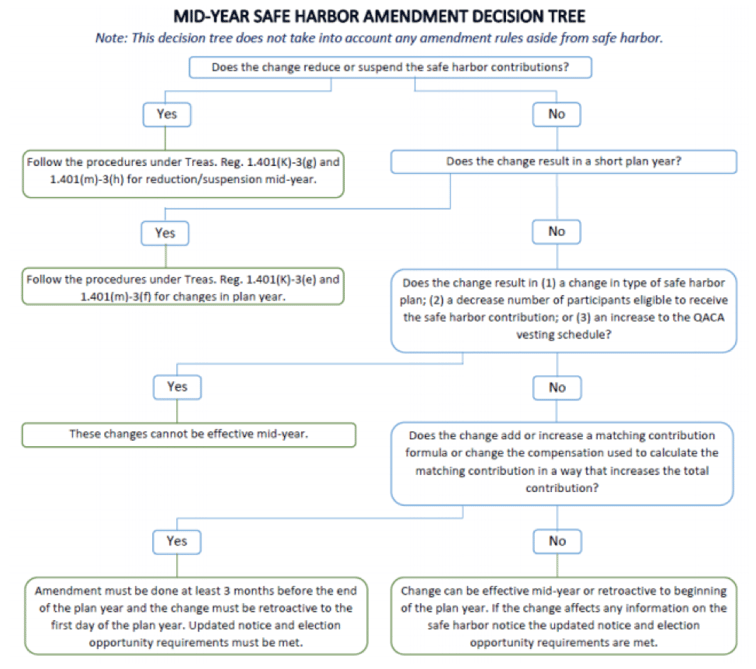

Special rules for safe harbor 401(k) plans

For a long time, safe harbor 401(k) plans could not be amended mid-year without causing the plan to lose its safe harbor status for the entire year. Notice 2016-16 changed that. Now, safe harbor status can be maintained if the following requirements are met:

- the mid-year change is not one of the prohibited changes listed in Notice 2016-16.

- If the change affects the information covered by the plan’s safe harbor notice, participants must receive an updated notice and the chance to change their deferral election.

- If the change increases safe harbor matching contributions, the mid-year amendment must be adopted at least three months before the end of the year.

Under a different IRS rule, employers are allowed to suspend or reduce safe harbor nonelective or matching contributions (as applicable) mid-year if either: (1) they are operating at an “economic loss,” or (2) the safe-harbor notice distributed prior to the start of the year states the following:

- The possibility that safe harbor contributions might be reduced or suspended mid-year,

- A supplemental notice will be provided if reduction or suspension occurs, and

- No reduction or suspension will take effect until at least 30 days after the supplemental notice is provided.

If a 401(k) plan is amended to suspend or reduce safe harbor contributions mid-year, the entire year becomes subject to ADP/ACP and top heavy testing.

Confused? Below is a decision tree that can help:

Source: ftwilliam.com

Amendments can’t cutback accrued benefits

401(k) plans are subject to “anti-cutback” rules that prohibit employers from reducing or eliminating benefits already accrued (earned) by participants by amendment. Common “protected” benefits include in-service distribution options (excluding hardships) and vested contributions.

Annual contribution allocations are also covered by the anti-back rules. Once a 401(k) participant satisfies the allocation requirements for a plan year contribution (e.g., 1,000 hours of service), their “allocable share” of that contribution can’t be reduced by mid-year plan amendment.

Non-protected benefits that can be reduced or eliminated by plan amendment at any time include plan eligibility, the right to make salary deferrals, and participant loans.

Correcting late amendments

A late amendment is considered a plan qualification failure by the IRS. That means doing nothing about the issue could potentially lead to plan disqualification. To correct a late amendment properly, employers must follow the terms of the applicable Employee Plans Compliance Resolution System (EPCRS) program:

- Self-Correction Program (SCP) - permits employers to self-correct certain plan failures without contacting the IRS or paying any fee.

- Voluntary Correction Program (VCP) - permits employers to, any time before an audit, pay a fee and receive IRS approval for correction of plan failures

- Audit Closing Agreement Program (Audit CAP) - permits employers to pay a sanction and correct plan failures found during an audit.

Late interim amendments can usually be self-corrected under SCP by adopting the amendment within a reasonable period after identification.

Staying out of trouble is easy with qualified help!

Hiring a quality 401(k) provider is critical to avoiding 401(k) amendment trouble easily. They will provide interim amendments automatically and prepare discretionary amendments on demand that won’t run afoul of IRS timing, safe harbor, or anti-cut-back rules.

That said, a quality 401(k) provider can only do so much. It’s up to employers to adopt the interim amendments they receive and to let their provider know when they are considering discretionary plan changes. A basic understanding of 401(k) amendments can help employers to do their part to stay out of trouble.