Login

Login

About 80% of our small business clients pay 100% of their 401(k) administration fees from a corporate bank account – not plan assets. I am confident that percentage is higher than average because most 401(k) providers don’t give 401(k) sponsors that opportunity. Instead, they force sponsors to pay at least a portion of their 401(k) admin fees from plan assets by limiting plan investment options to funds that pay them hidden 401(k) fees like revenue sharing and/or annuity wrap fees.

Because so few 401(k) providers offer plan sponsors the opportunity to pay 401(k) administration fees themselves, many business owners don’t know this option even exists. That’s too bad because it’s not just 401(k) plan participants that benefit when their employer pays 401(k) administration fees. Business owners also benefit by reducing their fiduciary liability, lowering their taxes, increasing their 401(k) returns and improving their plan’s attractiveness to employees.

Reducing 401(k) fiduciary liability

The #1 source of fiduciary liability for 401(k) plan sponsors today is paying excessive fees from plan assets. When 401(k) administration fees are paid from a corporate bank account – not plan assets – any potential liability for overpaying these fees is eliminated.

Lowering income taxes

When 401(k) administration fees are paid from plan assets, they are not tax-deductible. However, when a business pays them – they reduce the owner’s taxes. When a 401(k) plan is new, these fees may even qualify for a 50% tax credit – up to $5,500 for each of the first 3 years of your plan. Plan sponsors qualify for this credit when:

- They had 100 or fewer employees who received at least $5,000 in compensation in the prior year

- They had at least one plan participant defined as a non-Highly Compensated Employee

- It had been more than 3 years since they covered substantially the same employees under a different retirement plan

Increasing personal 401(k) returns

In many (if not most) small 401(k) plans, the business owner has the largest account balance. When this is the case, their account will pay a big chunk of any 401(k) administration fees paid from plan assets. Business owners can avoid this issue – and keep more of their retirement savings – by paying 401(k) administration fees from a corporate bank account. Due to the power compound interest, these annual savings can dramatically increase a retirement nest egg after decades of savings.

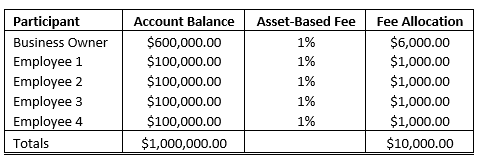

Example - assume a 5-participant 401(k) plan with $1M in total assets pays its 401(k) provider a 1% annual administration fee. If the business owner’s account balance is $600,000, they would pay 60% of the fee.

If business owner’s $6,000 fee remains in their account instead, it would grow to $48,987 in 30 years (assuming a 7% annual interest rate, compounded daily).

Improving 401(k) attractiveness to employees

Studies show many 401(k) participants are unclear regarding the fees paid by their account. That’s unfortunate given the erosive effect of 401(k) fees, but hardly surprising when you consider most 401(k) providers charge hidden fees that don’t appear in participant statements or fee disclosures.

However, it’s not hard for employees to understand that they’ll able to save more for retirement when their account is not reduced by 401(k) administration fees annually. This is a benefit employers can promote – making their plan a more attractive benefit to employees.

A win-win for both 401(k) participants and business owners!

In the past, business owners didn’t pay close attention to their 401(k) administration fees because they were buried in plan fund expenses and did not reduce their company’s bottom line. That’s changed. Due to DOL fee disclosure rules and several high-profile excessive fee lawsuits, most owners understand they risk personal liability by not understanding these fees and keeping them in check – an important fiduciary responsibility

The good news is that 401(k) providers are making it easier for owners to meet this fiduciary responsibility by charging only fully-transparent administration fees. Another virtue of these fees? They can be paid from a corporate bank account – not plan assets. When this is done, it can be a win-win for both 401(k) plan participants and the business owner.